29th Annual Masters of Logistics Survey: Are we ready to change?

While technology is a key part of digital transformation in logistics and transportation, strategy, structure and processes must be aligned accordingly to create value for the company and its supply chain partners.

Digital Darwinism suggests that companies were historically designed to evolve and improve over time, but that things are different now. The speed of technological and societal change no longer affords companies the luxury of slow incremental improvements or adaptations. Instead, companies must look forward and dare to ask the hard question: Are we willing to change?

The “29th Annual Study of Logistics and Transportation Trends” posed these questions to over 290 logistics and transportation professionals to gain added insights into how their organizations are responding to the disruptive pressures of new technology, rising customer expectations, and a global pandemic. The study revealed a number of new insights.

“Digital technologies alone provide little value to an

organization.”

While technology is a key part of digital transformation in transportation, strategy, structure and processes must be aligned accordingly to generate new ways to create value for the company and its supply chain partners.

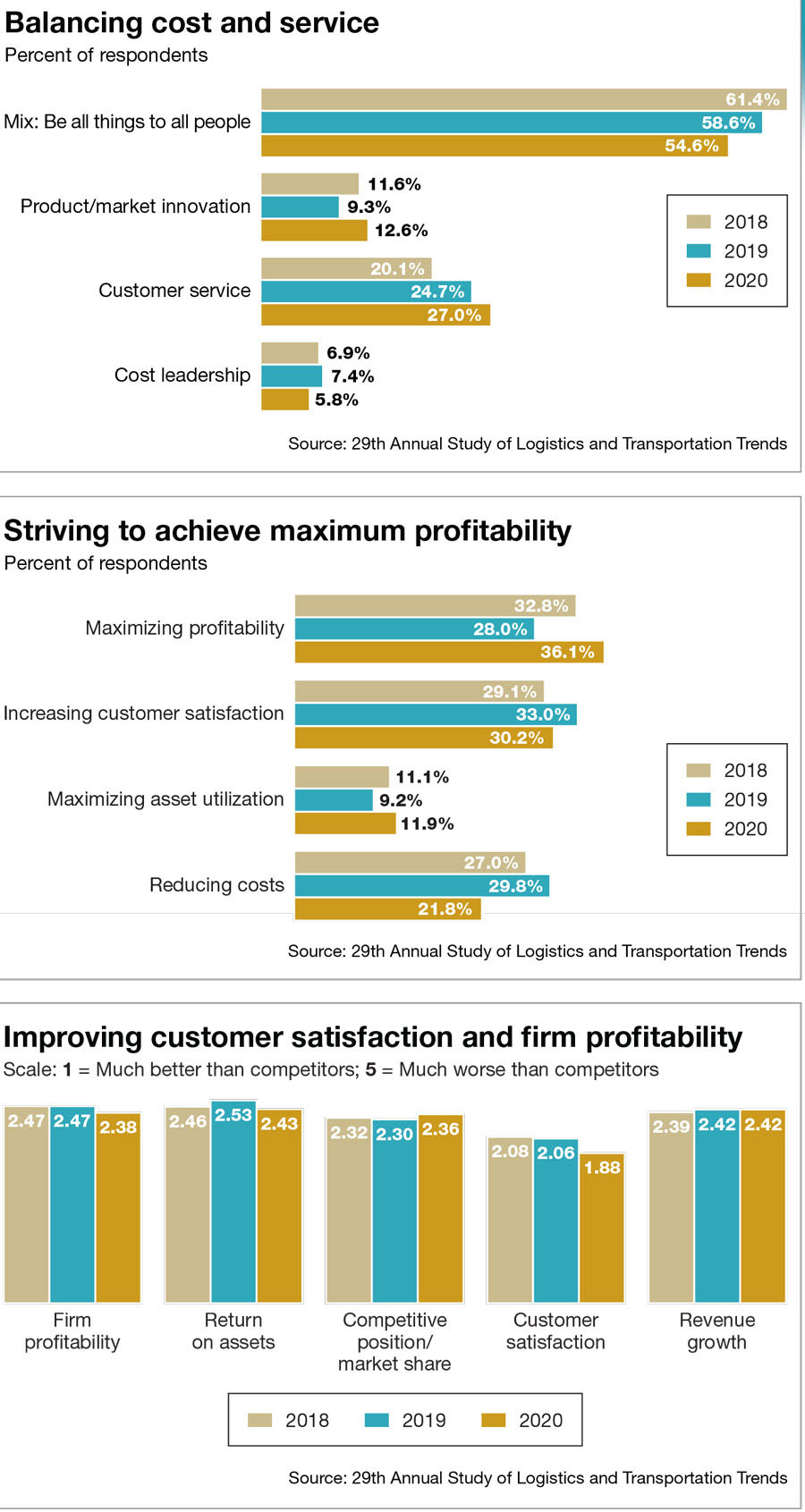

A little more than 54% of the respondents described their strategy as a mix between balancing cost and service objectives (“being all things to all people”). In theory, this policy allows a company to offer a bundle of products or services that are specific to a customer or customer groups.

From a logistics and transportation perspective, differentiated service is a means of creating value. In practice, the mix strategy is often difficult to conceive or operationalize. In order to be effective, the front-office interface with the customer must be fully integrated with the back-office internal support activities and systems. Unfortunately, many companies still struggle with seamless integration—a key factor in our quest for a digital supply chain.

In the past three years, two competing objectives—increasing customer satisfaction and reducing costs—tended to dominate tactical and operational decisions. However, in 2020, the goal of “maximizing profitability” was the primary objective for approximately 36% of our respondents, an increase of nearly 29% over last year’s data.

In contrast, increasing customer satisfaction and reducing costs both declined, -8.5% and -18.9% respectively. We believe this shift highlights the growing focus on cost to serve and use of technology to gain operational efficiencies while meeting rising

customer expectations.

Why is this alignment important? It has a bearing on company performance. The results of our 29th annual study seem to confirm this association. Over the past five years, respondents report their company performance across key measures of profitability, return on assets (ROA), market share, customer satisfaction, and revenue growth have been stagnate as compared to their competitors.

In 2020, firms focused on customer satisfaction reported a significant improvement from the previous years, with ROA and firm profitability also increasing relative to competitors.

Fundamental service performance is lagging

To achieve the desired performance outcome, it’s not sufficient to only have alignment of strategy with the logistics and transportation objective. The objective must be the driving force behind decisions that are made in day-to-day operations.

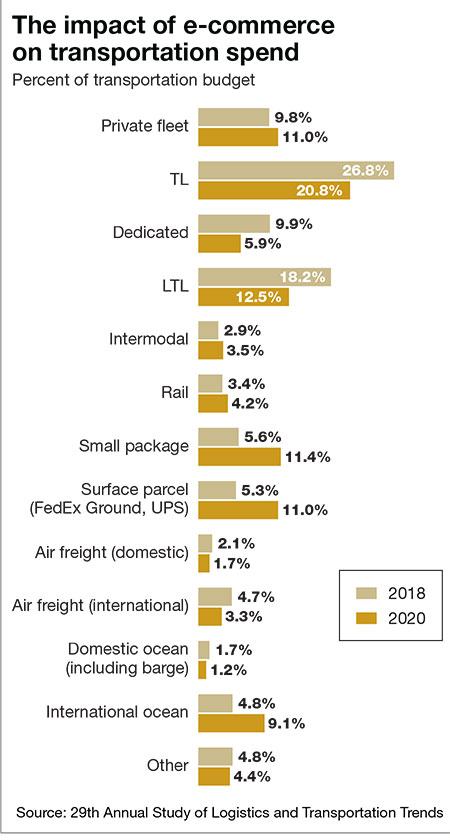

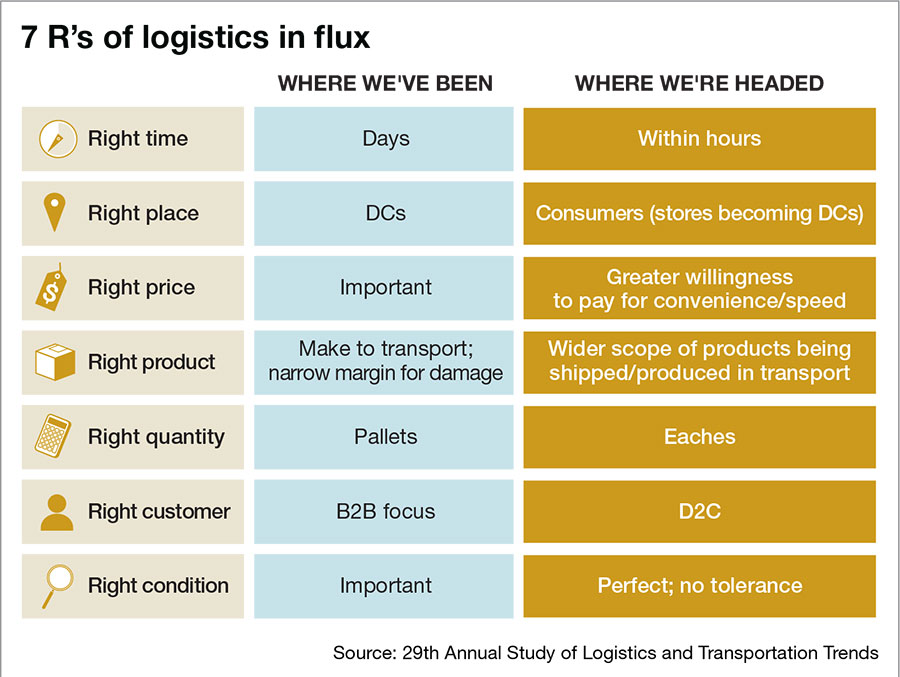

One of the structural components of transportation decision-making is how to move freight. The double-digit percentage growth in e-commerce market share is reflected in a significant shift in transportation spend by mode. A comparison of 2018 to 2020 data indicates that small package and surface parcel have doubled their share of the transportation budget during this time frame. The gain in these modes occurred at the decline of transportation spend for truckload (TL), less than truckload (LTL) and dedicated truck.

Consumer expectations regarding delivery are rapidly changing: Same-day delivery is the fastest growing option for expedited service. In addition, consumers want to know where their shipment is in the fulfillment process and when they can expect to receive it. In fact, a vast majority of consumers expect that they will be able to track their shipments in real time. This level of service places a tremendous amount of pressure on transportation providers and upstream supply chain members to achieve that goal.

Consumer expectations regarding delivery are rapidly changing: Same-day delivery is the fastest growing option for expedited service. In addition, consumers want to know where their shipment is in the fulfillment process and when they can expect to receive it. In fact, a vast majority of consumers expect that they will be able to track their shipments in real time. This level of service places a tremendous amount of pressure on transportation providers and upstream supply chain members to achieve that goal.

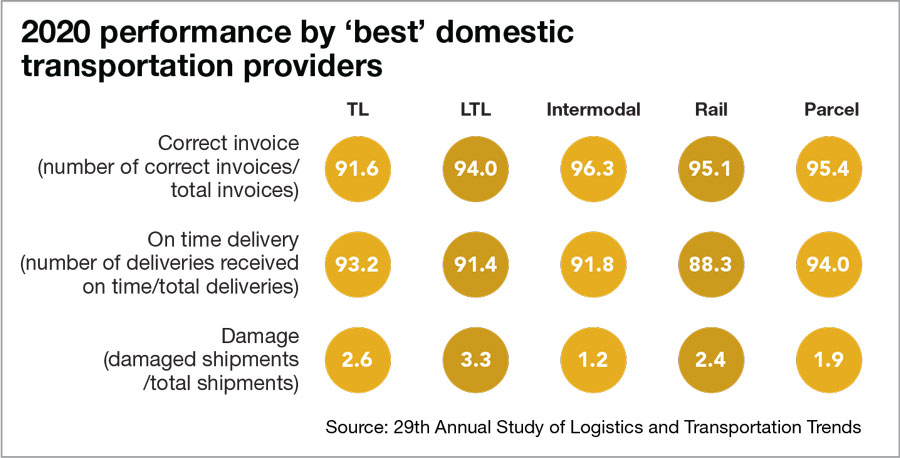

Data from the annual study indicate that transportation providers are not meeting expectations for several elements of service including on-time delivery. Parcel, which is a primary mode for next-day and same-day deliveries, reported a 94% on-time delivery rate for 2020.

LTL, which also plays a key role in e-commerce freight, posted an on-time delivery score of 91.4%. In global supply chains that run lean on inventory, keeping damage rates low is important. In 2020, LTL recorded the highest level of damage followed by TL and rail. Except for rail, the rate of damage for the five modes—TL, LTL, intermodal, rail and parcel—are the highest reported over the past five years.

Clearly, there’s ample opportunity to improve on these service elements that are considered to be fundamental performance measures.

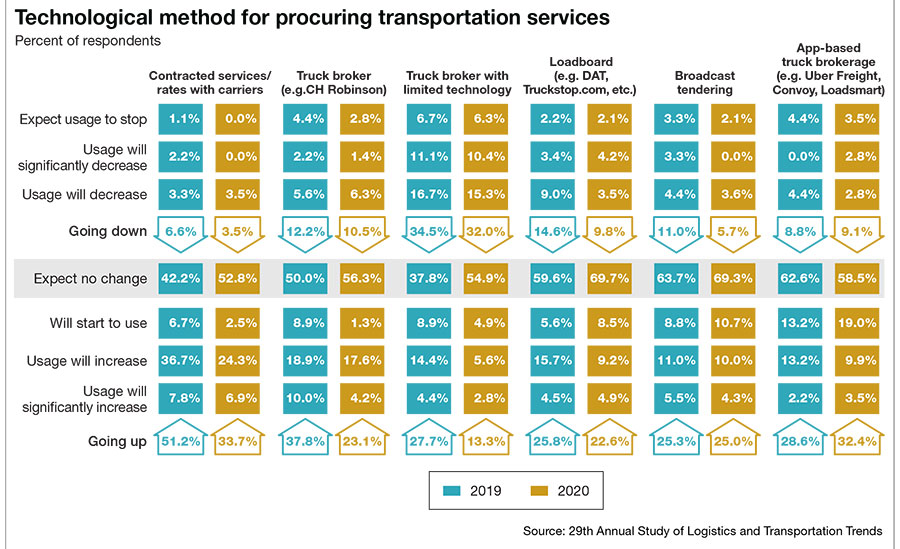

We found that transportation services are being procured by shippers using a variety of methods, from traditional contracts to app-based truck brokerage. In a business environment where the rate of change and technology adoption is occurring at a pace faster than ever, it’s interesting to note that very little change is anticipated in the transportation procurement process.

A comparison of 2019 to 2020 data highlights some interesting findings. First, compared to 2019, the majority of respondents expect no changes in how they procure transportation services in 2020.

In fact, respondents were more tied to the status quo for all methods except for app-based truck brokerages, which saw a small decline in “expect no change,” but a 13% increase in expected growth or usage. Second, all of the methods show continued growth—that is, increased use exceeds usage going down—in all cases but one: brokers with limited technology.

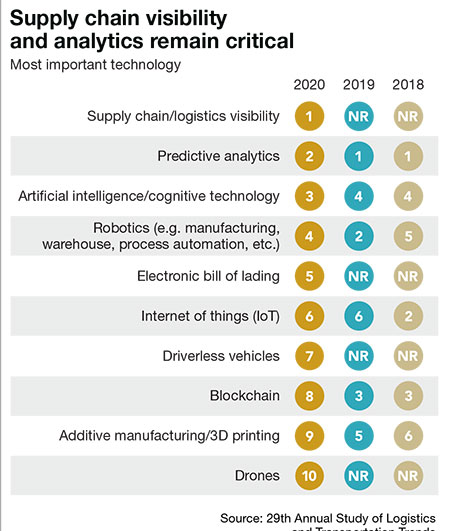

Of all the things that have changed, the need for visibility remains constant. As noted below, respondents rank visibility as the most important technology for the next three years. For large firms—the Masters—visibility and predictive analytics were both equally ranked as most important, followed by artificial intelligence and cognitive technology.

For small firms (annual revenue less than $500 million), their third ranked choice was more operational: an electronic bill of lading. What makes this more interesting is that respondents seem to think that customer expectations for real-time visibility is greater than what is currently possible.

What’s interesting about the continued importance of visibility is that, overall, it has increased over the past two decades. Dick Tracy’s watch phone has rung to life. Knight Rider’s Kit is more real than imagined. The robot in Lost In Space would be at home in many DCs today. Yet, at this time of great technological advances, there is a need for more.

Searching for meaning

What does it all mean and what do we do now?

What does it all mean and what do we do now?

All of these changes point to one thing: the increased need for timely information. Information is becoming, as one respondent we interviewed noted, “table stakes to enter the game.” Walter Wriston, the former CEO of Citicorp, once wrote: “Information about money has become almost as important as money itself.”

For a more effective and efficient flow of goods, supply chain information needs to move seamlessly across company boundaries. This will require greater intragration (internal to the firm) and integration (across the supply chain). Having the information is only part of the equation: firms will have to execute using it.

This is not a challenge that can be accomplished by a single carrier, let alone a single shipper. Working on the edges will not get the productivity gains needed. Rather, it will require a collaborative network—closed or open—of shippers and carriers working together on a single platform.

Digital direction

This points to, perhaps, the greatest untapped opportunity for the managers in the logistics and transportation industry. Will we create, support or partner to create collaborate networks of firms to manage the 2.3 million trucks running empty 25% of the time? Or, more precisely, is the digital freight network right around the corner?

The digital direction has to be focused internally and externally. While firms have worked to minimize costs and maximize efficiency, they have done so based on their own single network.

If information were more ubiquitous and available, shippers and carriers could work together to reduce costs, become more sustainable and increase profitability.

Getting ready for the digital redefinition of transportation starts with the right mindset. It starts with understanding that the road to riches has changed as well as the understanding that the digital redefinition of transportation requires the right tools. APIs, TMS, eBOLs, AI, machine learning and a dozen other technologies not only need to be part of the conversation: they need to be part of our processes.

Also, the digital redefinition of transportation requires the right partners. Some firms will stay analog, assuming past success will lead to future success. This is partially correct, in that they will serve a market, but one that is ever-decreasing in size.

We too have seen the slow change and adoption of technology in the discipline. The interconnectedness of all of the modes, technologies and people can make any significant changes slow to implement. However, for some companies, these changes present an opportunity to gain competitive advantage as they pivot to establish themselves as digital front runners in the redefinition of transportation.

Article Topics

Motor Freight News & Resources

Shipment and expenditure decreases trend down, notes Cass Freight Index March trucking tonnage trends down, reports ATA FTR Shippers Conditions Index enters negative territory DAT March Truckload Volume Index sees modest March gains National diesel average, for week of April 22, is down for the second straight week LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics XPO opens up three new services acquired through auction of Yellow’s properties and assets More Motor FreightLatest in Logistics

Understanding the FTC’s ban on noncompetes UPS rolls out fuel surcharge increases U.S. rail carload and intermodal volumes, for week of April 20, are mixed, reports AAR Baltimore suing ship that crashed into bridge, closing port, costing jobs Intermodal growth volume remains intact in March, reports IANA Descartes announces acquisition of Dublin, Ireland-based Aerospace Software Developments Amid ongoing unexpected events, supply chains continue to readjust and adapt More LogisticsSubscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources