State of Logistics 2021: Truckload

Carriers flush with freight, but high equipment, driver costs strain profits.

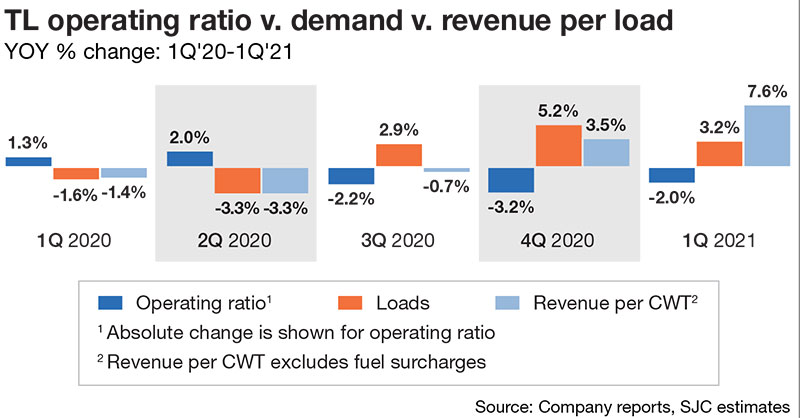

Truckload (TL) Carriers are battling strong demand for capacity with sharply higher costs for everything from raw materials for their trucks to rising driver pay.

“Fleets simply need more trucks and trailers,” says Don Ake, vice president of commercial vehicles for research firm FTR. In fact, the demand for Class 8 heavy trucks could be more than 325,000 units this year. “But we don’t know because supply is constrained,” he says. “That demand could spill over into 2022.”

As for overall conditions in the $340 billion TL sector, where the top 25 carriers combined barely have a collective 10% market share, Ake contends: “It’s a tough market, and it could get even tougher.”

The DAT spot market indicator showed TL rates remained near all-time highs during the week ending May 3, one year after bottoming out as U.S. economies closed during the pandemic. The seven-day average line-haul rate for dry van was $2.27 a mile in early May, which is 95 cents higher than the same period one year ago. Contract rates nearly always follow the spot market.

FTR is predicting 4.4% growth in gross domestic product (GDP) in the third quarter and another 2.4% in the fourth quarter of 2021, compared with a pandemic-constrained GDP a year ago. There was a stunning 17.4% rise in goods transport growth in the first quarter year-over-year that got the nation back to where we were last year.

Although some supply chain issues persist—computer chips for Class 8 trucks and lumber for floors of trailers—at least 20 different suppliers on the heavy truck side are facing shortages in areas of rubber, plastic resins and specialized steel. All this is crimping delivery of new Class 8 trucks, and is now affecting how many new trucks are on the highway.

“It’s a great time to have trucks, and it’s a great time to have new trucks,” says Derek Leathers, vice chairman, president and CEO at Werner Enterprises, the nation’s 7th-largest truckload carrier.

According to reports, carriers need to be prepared to pay more for trucks. Specialized steel was less than $500 a ton last year. This year, steel spiked to nearly $1,400 a ton. The same thing is happening with rubber. Monthly rubber prices were $1.32 per kilo last year and rose to $2.35 this year—nearly doubling within a year.

Still, TL carriers are placing orders for heavy trucks. Carriers recently posted six straight months with more than 40,000 Class 8 orders per month. “Now you have restricted supply not being able to keep up with demand,” says Ake. And even with current supply chain constraints, FTR is forecasting total Class 8 production of 310,000 this year, 340,000 for next year and 350,000 for 2023.

“Freight growth in 2021 and 2022 will continue to put the industry in catch-up mode,” Ake predicts. “We’re in the midst of three super years for the industry as we recover from the problems of 2020.”

The good news for truckload carriers is that the OEM community is optimistic they can meet demands, and the Class 8 heavy truck supply chain is rebounding. However, reports indicated that supply chain issues remain.

While there may not be shortages forever, high raw material costs are boosting prices for new Class 8 trucks. “The high component and material costs are squeezing margins on OEMs this year,” adds Ake. “They’re building more, but their margins are squeezed.”

Learn about the additional State of Logistics topics here.

Article Topics

Latest in Logistics

April Services PMI contracts after 15 months of growth, reports ISM 2023 industrial big-box leasing activity heads down but remains on a steady path, notes CBRE report U.S. rail carload and intermodal volumes are mixed in April, reports AAR Q1 U.S. Bank Freight Payment Index sees shipment and spending declines S&P Global Market Intelligence’s Rogers assesses 2024 import landscape Pitt Ohio exec warns Congress to go slow on truck electrification mandates Q1 intermodal volumes are up for second straight quarter, reports IANA More LogisticsSubscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

May 2024 Logistics Management

Latest Resources