State of Logistics 2021: Rail/Intermodal

Volumes remain strong, but keep a watchful eye on service.

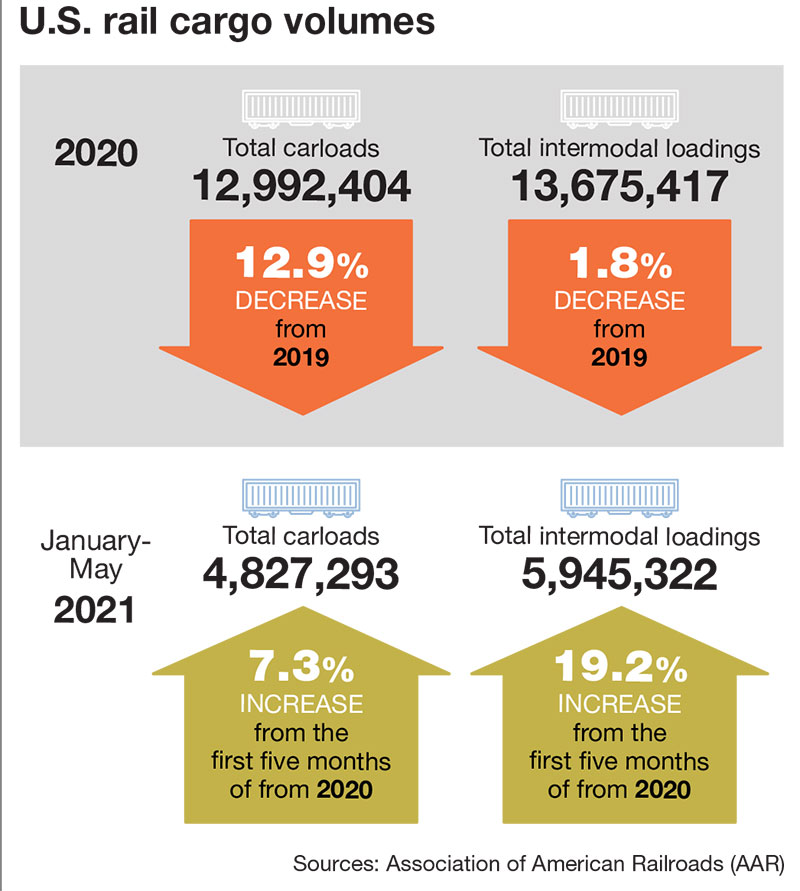

A year ago, the impact of the pandemic had knocked a serious dent into the state of U.S. rail carload and intermodal volumes. But today, volumes are recovering at a significant pace due to the vast differences in business conditions between the two periods of time.

According to data from the Association of American Railroads (AAR), U.S. carload volumes are up 7.3% through the first five months of 2021 on an annual basis. And the weekly carload average for May far outpaced the May 2020 weekly carload average, which AAR said represents the lowest ever recorded since it started tracking this data in 1989. For the month of May 2021 alone, U.S. rail carloads saw a 30.4% annual gain, according to AAR.

Meanwhile, rail intermodal volumes have also shown a strong rebound compared to a year ago, with May U.S. container and trailer volume seeing a 26.2% annual increase. And U.S. container and trailer volumes through the first five months of 2021 are up 19.2% annually. Average U.S. weekly intermodal volume for May showed a 20.7% annual increase.

What’s more, according to AAR data, this marks the 7th-highest weekly U.S. intermodal average for any month, and the most ever for the month of May.

“U.S. rail volumes in May 2021 were encouraging,” says AAR senior vice president John Gray. “Total carloads were the most for any month since October 2019 on a weekly average basis. In May, 18 of the 20 carload categories we track had carload gains over May 2020, while 12 of the 20 had gains over May 2019. Meanwhile, intermodal just had the best January to May period ever for U.S. railroads.”

While the volume gains are a good sign for freight railroad and intermodal, Tony Hatch, principal of New York-based ABH Consulting, describes the annual comparisons as almost meaningless due to how 2020 volumes were negatively affected by the pandemic.

“Not only did the pandemic and the effects of the Polar Vortex impact conditions in the first quarter, unusual weather is much more usual when it happens year-over-year,” says Hatch. “Another thing to remember is that 2019 was a bad year for railroads, as we were—and still are—in a trade war, with tariffs still on almost $400 billion worth of goods.”

Over the course of the ongoing economic recovery, Hatch noted that railroads have done an exemplary job going back to the second half of 2020, adding that even though some cracks are beginning to show a little bit, he says that railroads are not the main offenders in the supply chain compared to ports, for example, which dealt with major congestion issued earlier this year.

“I would give the rails an A- or a B+ for the second half of last year and a B for the first part of this year,” says Hatch. “Hopefully, that is not a trend. There are some stresses, like pressure on intermodal, due to the truck driver shortage. That is a good thing for business in some ways, but it’s also hard with rails having a tough time getting crews.”

While railroad and intermodal volumes are strong, Hatch says that a watchful eye needs to be kept on service in the wake of a recent letter from STB chairman Martin Oberman to leadership at Class I railroads. The letter was in regards to rail service issues reported by some shippers, adding that it may relate to a broader trend of rail labor reductions over the last several years, coupled with the pandemic-driven furloughs and quarantines.

“This letter sends signals to the railroads that the STB is not happy with them,” adds Hatch. “I would argue that the STB comes with a preconceived notion to not be happy regarding service, and that shippers want to look unhappy so prices are down and it lowers logistics costs.”

Learn more about the latest State of Logistics updates here.

Article Topics

Rail & Intermodal News & Resources

U.S. rail carload and intermodal volumes are mixed in April, reports AAR Q1 intermodal volumes are up for second straight quarter, reports IANA 2024 State of Freight Forwarders: What’s next is happening now STB announces adoption of final reciprocal switching rules Norfolk Southern-Ancora Holdings proxy battle accelerates Intermodal growth volume remains intact in March, reports IANA Shipment and expenditure decreases trend down, notes Cass Freight Index More Rail & IntermodalLatest in Logistics

April Services PMI contracts after 15 months of growth, reports ISM 2023 industrial big-box leasing activity heads down but remains on a steady path, notes CBRE report U.S. rail carload and intermodal volumes are mixed in April, reports AAR Q1 U.S. Bank Freight Payment Index sees shipment and spending declines S&P Global Market Intelligence’s Rogers assesses 2024 import landscape Pitt Ohio exec warns Congress to go slow on truck electrification mandates Q1 intermodal volumes are up for second straight quarter, reports IANA More LogisticsAbout the Author

Subscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

May 2024 Logistics Management

Latest Resources