This year’s recent TPM – the annual transpacific maritime conference hosted by the Journal of Commerce in Long Beach, CA at the end of February – was a combination of post-pandemic debrief, projections for the rest of the year and beyond, and lessons learned.

There were plenty of freight insights to take in over three days of sessions, meetings and conversations with carriers, forwarders and BCOs, but far too many to include all of them in a blog post that anyone might make it to the end of. So, here are some of the highlights.

Overall, as ocean spot rates suggest, the sentiment was that things are finally heading back to normal though accompanied by a healthy dose of uncertainty as shake ups in carrier alliances and strategies, a looming surge of new vessels adding capacity to the market, and economic wildcards that could impact consumer demand make the future somewhat murky.

What just happened???

In the debrief department, Sea Intelligence’s Alan Murphy shared data confirming that – of course – surging demand was the trigger for the unprecedented ocean situation.

But it was the record number of vessels that carriers shifted to satisfy the demand that caused the congestion – which, as Wan Hai’s Vice Chairman, Randy Chen put it, “broke the system” – which was the actual big driver of extreme rates and dismal reliability.

As volumes and congestion have eased though, Sea Intelligence data shows that reliability is improving (though with about 50% of ships arriving on time, things are still not great compared the 80% pre-pandemic norm) and utilization levels are back to pre-pandemic levels which in turn are driving the decrease in rates.

What happens next?

Ocean freight maven Lars Jensen of Vespucci Maritime encouraged attendees not to fear: He sees the last years as remarkable, but also views the current ocean environment as quite normal in that recognizable ocean freight market dynamics are back to determining the market’s trends.

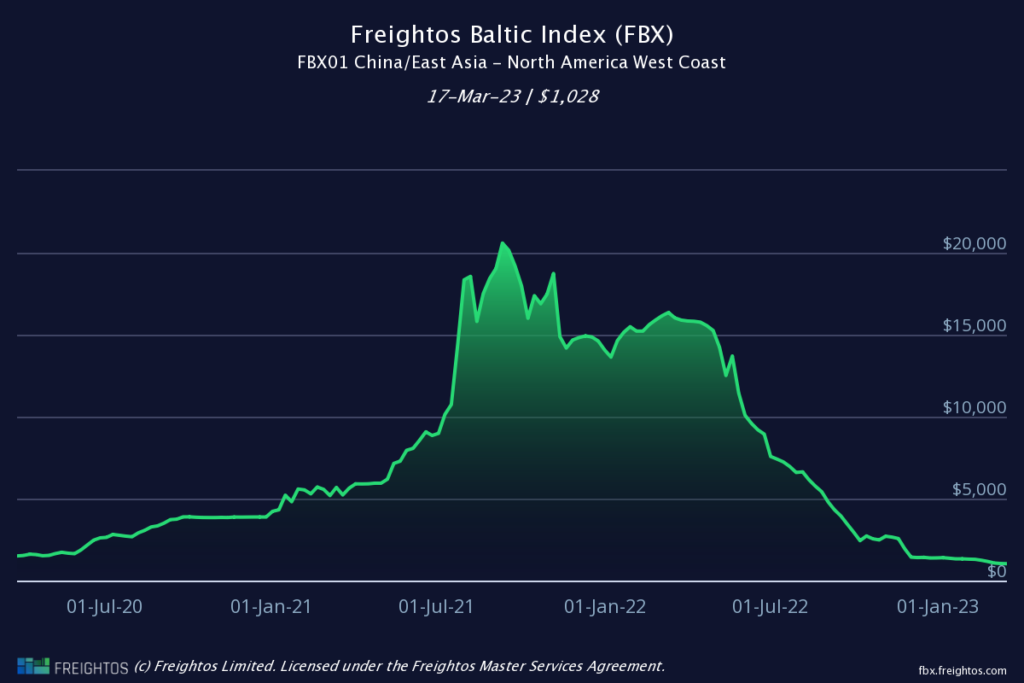

Rates are falling back to pre-pandemic levels or below – transpac rates to the West Coast approaching just $1,000/FEU, lower than any point in 2019 – because the market is now in a down cycle, just like it has been many times in the past after an inventory build up and before an inventory correction.

The downturn may be painful (for some), but is not unusual.

The current environment of excess capacity and rate war stands in contrast to early 2020 when volumes sank but carriers removed enough capacity via extensive blanked sailings to keep rates from crashing.

But with inventories still high, volumes low and carriers – in the bumpy “period of instability” ahead of alliance shake ups – with cash reserves to support a push for market share, carrier decisions (based on shifting strategies) to keep more capacity active this time around has a logic too.

Jensen thinks carriers are willing to compete relatively strongly on price until the most likely (though not certain) scenario of rebounds in demand and rates starting in the spring.

Anja Roennfeldt, EVP of Ocean Freight at DB Schenker shared that part of carrier hesitancy to blank as extensively as last time is driven by the desire to provide better reliability and service to their customers now that they can. This move is in the hopes of building loyalty from shippers (perhaps especially after the last few years of delays) even at the cost of lower rates – for now.

Complicated time for contracts

Other experts expressed how current rate levels are also seen as complicating long term ocean contract talks, many of which were taking place during TPM.

Robert Khachatryan, CEO of Freight Right, a US-based forwarder whose services are available through the Freightos.com marketplace, reports that “carrier representatives were hinting at about the $1,800-$2,000/FEU range for West Coast volumes and $3,000 – $3,200 to the East Coast.”

But with spot prices well below that level – and still falling – this target is likely unrealistic to most shippers. The largest importers – whose contracts generally determine the benchmark for other BCOs each year – have yet to sign.

Khachatryan continued that “it is probably reasonable to expect that contract rates for mid-size forwarders and mid/large BCOs will end up being around $1,500-$1,600/FEU for the West Coast and $2,500-$2,700/FEU to the East Coast.”

Contracts signed above current spot-levels would probably reflect a few realities: Carrier costs have gone up with inflation, and current spot rates are below break-even for the box lines. As contracts run from May to May, contract rates of $1,500+ may also reflect both carrier and shipper optimism for an H2 rebound in volumes and higher rates into 2024.

On the flipside, these rates may also signal that – in the absence of a volume recovery and/or if too large a share of volumes opt for the spot market over contracts – carriers will remove enough capacity to push rates up to profitable levels anyway, a move taken in early 2020 but so far avoided in the last few months.

BCOs agreeing to these contract rates might also show that some importers are willing to pay something of a premium for better reliability. Meanwhile, shippers who manage to sign contracts nearer current market rates may be at risk of seeing those volumes get rolled for more lucrative spot containers if spot rates indeed climb high enough.

So these long term contract negotiations are taking place with more explicit recognition that contracts are inherently flawed.

Research we conducted in 2021 showed the impact that pandemic-driven rate volatility had on both forwarders and shippers – in terms of increases in contracted volumes getting rolled, ad hoc premiums added, or carrier requests for renegotiations – as spot rates spiked. Meanwhile, after shippers pushed to sign new – more expensive – contracts for 2022 in the hopes of ensuring better reliability, spot rates plummeted in the second half of that year and the cycle restarted in reverse with shippers abandoning contracts for spot or pushing carriers to renegotiate.

Ocean contracts can now be linked to reliable benchmarks like the Freightos Baltic Index, removing the incentives for price-based disruptions like when contract and spot levels get out of sync. And the exposure to index-linked price fluctuations can be managed through new freight futures agreements, now tradeable on both the CME and the SGX.

Jensen noted that the ocean contract experience of the last couple years will likely push more shippers to these new types of contracts, and Nigel Pusey of Container Trade Statistics remarked that – on Asia-Europe lanes, at least – we may see more index-linked contracts this year as shippers look for better reliability. Conversations with major BCOs also pointed to interest in these types of better contracting solutions, even if the industry is still in the early days of this shift.

More (too much?) capacity on the way

Alphaliner Senior Analyst, Jan Tiedemann, provided data and context on the magnitude of the new vessel order book slated to enter the market over the next few years. (My favorite: MSC’s orders are equal in size to Hapag-Lloyd’s current active fleet.) He also laid out that global capacity has grown linearly over the past twenty years even through ups and downs in demand on specific lanes resulting in overcapacity.

The mitigation strategies – slow steaming, scrapping, reduction in charters, and deferrals of new orders – do not appear to be enough to prevent overcapacity given projections for demand levels. But Tiedemann also pointed out that carriers have this information too – with many continuing to place orders even when demand was already waning – and are nonetheless bullish on new capacity working in their favor either in terms of new strategies relative to alliances or optimism for growth in new developing markets.

Along those same lines, remarks from MSC’s CEO Soren Toft included projections that global volumes will climb back to 2021-2022 levels within the next four years, and therefore carriers will need the capacity to serve that market. But he warned that ports may not grow at the same pace to accommodate those volumes, which could slow container flows and – together with the cost of becoming more green also being passed on to shippers – push rates up.

Tech to save the day?

Finally, tech also played a more prominent role in the narrative than it has in the past. Many in the industry viewed the pandemic as a catalyst for tech adoption in freight, and think the easing of operational pressure will lead to more focus on neglected digital initiatives.

In addition to digital connections that can facilitate operational aspects like tracking visibility and eBooking, or pricing visibility that can help shippers or forwarders make better spot decisions or more reliable contracts, CN CEO Tracy Robinson explained that “no one wants to be surprised.” And the way to avoid surprises is through better data and better data sharing.