SONAR data show that the freight market for inbound Detroit loads is highly volatile based on auto production trends – inbound Detroit loads should be less expensive when OEMs are sourcing a lot of components as assembly volumes ramp up. Conversely, it is easier for auto companies to source components into Detroit at lower freight rates when production levels decline.

Due primarily to the global semiconductor shortage, automotive production is one area of the economy that has not recovered from the COVID recession.

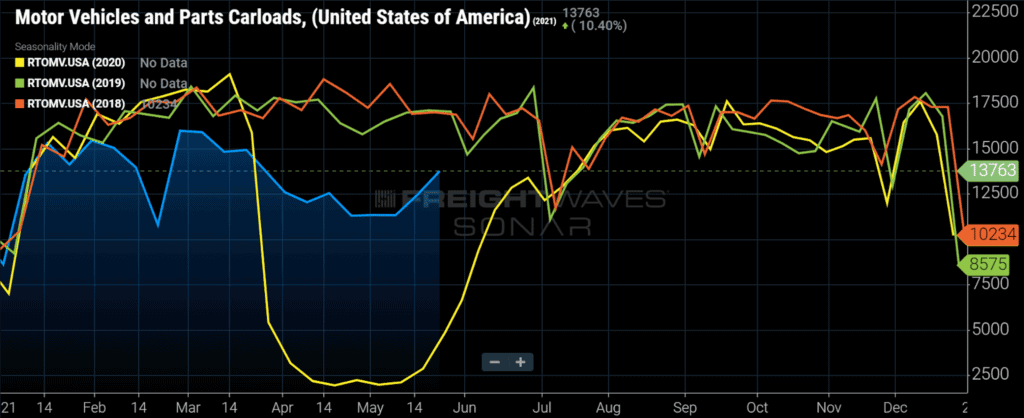

In 2020 (yellow line below), automotive rail carloads, which primarily consist of finished vehicles, fell off a cliff in March before recovering to seasonal norms in July. 2021 volumes (blue line) remain significantly below 2018 and 2019 levels due to the ongoing semiconductor shortage. Its impact is magnified the longer the shortage persists because there is a certain amount of vehicle replacement that needs to take place each month (~1.4 million units +/-) as vehicles are taken out of service.

Motor vehicle shipments on the Class I railroads are shown for 2021, 2020, 2019 and 2018 in blue, yellow, green and orange, respectively. (Source: SONAR)

The volatility in the auto industry has wreaked havoc on the Detroit freight market.

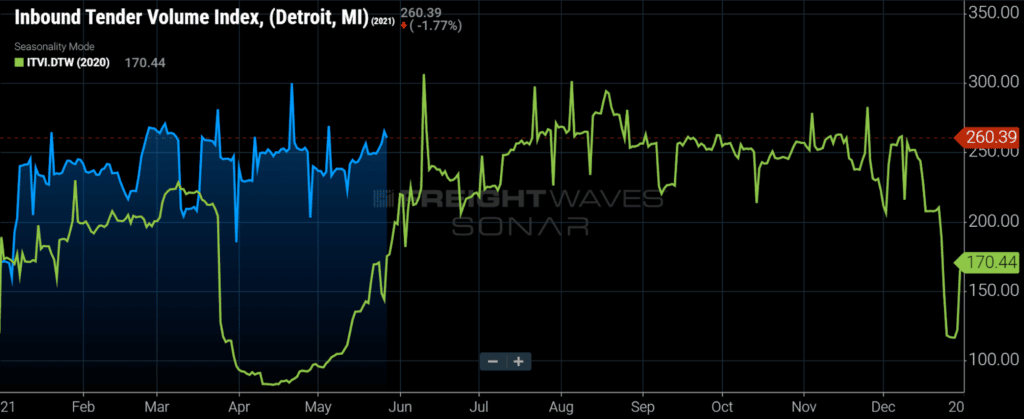

Demand to move truckloads (which presumably includes many truckloads full of auto parts) into Detroit fell sharply in March 2020 amid plant shutdowns before an acceleration in inbound freight demand as production came back online in 3Q20.

(Source: SONAR)

Detroit is typically a backhaul freight market, but the severity of the freight imbalance changes dramatically with market conditions.

There is typically more demand for inbound truckloads into Detroit than outbound truckloads. That is due to the consumption in the area and also because a large volume of auto parts are hauled by truck into Detroit while finished vehicles typically leave in rail carloads, at least those traveling long distances.

While Detroit’s status as a backhaul market didn’t change during the COVID era, the magnitude of its freight imbalance changed dramatically. When auto plants shut down in late March 2020, Detroit’s freight market became balanced with roughly an equal volume of inbound and outbound freight tenders (a measure of freight demand), simply because the region wasn’t demanding as many inbound auto parts as it typically does. That’s important information for shippers that are moving goods that terminate in Detroit because it means that they have more negotiating leverage with carriers (since carriers can get re-loaded in Detroit more easily).

Of course, the auto plant shutdowns last year didn’t last long and the region became a severe backhaul market by July and August as OEMs demanded large volumes of inbound components and production schedules attempted to make up for lost time. During periods with those characteristics, shippers often struggle to secure capacity and it is often a good idea for shippers to make sure routing guides are in order and to extend lead times to help secure capacity.

Detroit briefly became a balanced market in April 2020 (Detroit Headhaul Index near zero) before returning to its typical backhaul status.

An indicator of balance (or imbalance) in freight demand, the Detroit Headhaul Index subtracts inbound demand from outbound demand. Deeply negative numbers indicate that there is greater inbound truckload demand than outbound truckload demand. (Source: SONAR)

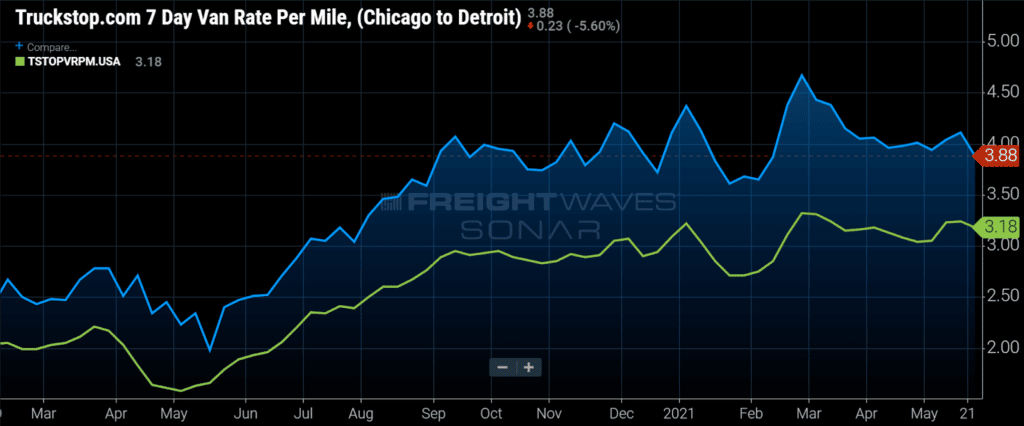

Carriers’ reluctance to head to Detroit (a backhaul market) explains why rates on loads inbound to Detroit are typically priced at a premium to most other lanes.

The chart immediately below compares spot rates from Chicago to Detroit ($3.88/mile, including fuel surcharges) to the nationwide rate of $3.18/mile, which also includes fuel surcharges. While tender rejection rates (second chart below) show carriers’ reaction to the market conditions and the chance that shippers’ tenders are accepted, spot rates, such as those shown below, help shippers quantify the magnitude of risk in the event that loads fall through the routing guide.

(Source: SONAR)

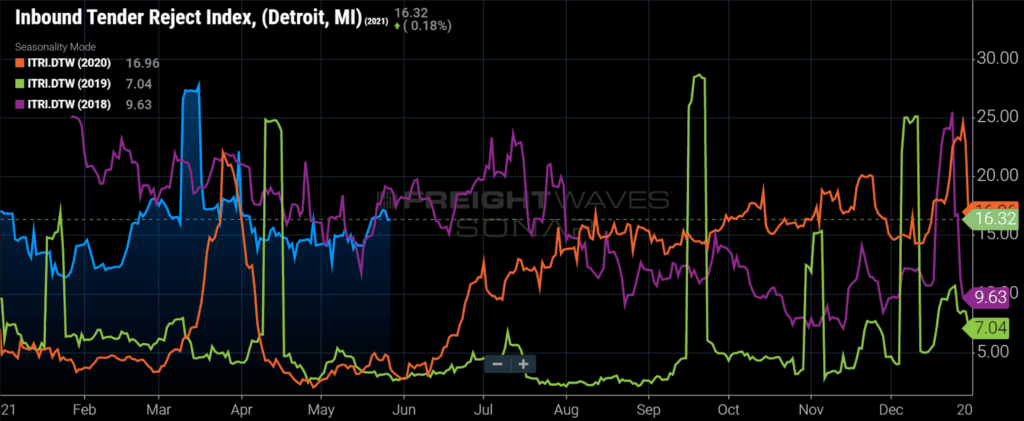

Carriers are responding to the freight market for inbound Detroit loads, similar to the way they did in spring/summer 2018, by rejecting about 16% of tendered loads.