The finished vehicle sector in North America is dealing with a lot of challenges at the moment. There is a basic imbalance in the number of vehicles that the US imports and exports with its global trading partners, which contributes to ongoing problems involving congestion and limited capacity on hinterland feeder services, something compounded by a lurch in consumer preferences for bigger trucks and away from passenger vehicles (sedans). That, in itself, is being influenced by the US government’s revision of policy on emission standards.

The finished vehicle sector in North America is dealing with a lot of challenges at the moment. There is a basic imbalance in the number of vehicles that the US imports and exports with its global trading partners, which contributes to ongoing problems involving congestion and limited capacity on hinterland feeder services, something compounded by a lurch in consumer preferences for bigger trucks and away from passenger vehicles (sedans). That, in itself, is being influenced by the US government’s revision of policy on emission standards.

At the same time, the government, under President Trump, seems hell-bent on a trade war with China (and anyone else) and is renegotiating the 24-year-old Nafta agreement with its closest trading partners, both of which carry threats of 20%-plus import tariffs. And finally, port infrastructure for finished vehicle handling is still in need of some major investment.

Given all this uncertainty and what it means for the business of moving finished vehicles to and from the ports in North America, it was helpful of Kirk Claussen, port finance agent in the Office of Ports and Waterways at the US Maritime Administration (Marad), to start proceedings at this year’s Finished Vehicle Logistics Import Export summit in Baltimore with a couple of simple definitions.

“The purpose of a port is for the direct intermodal exchange of people or freight,” he said, adding that ports should have the infrastructure to allow vehicles and trains to come alongside ships.

For Claussen, it is crucial that those ports have the necessary infrastructure to cope with the continued growth in global trade. The US vehicle handling ports exported 4m vehicles last year and imported twice that number, according to data from analyst PwC.

Claussen admitted that congestion was increasing because the port infrastructure coping with multiple types of cargo had limited capacity, including the landside road and rail links, which took decades to expand. At the same time, however, there are 25,000 miles of coastal and inland waterways that are underused.

Kurt Nagle, CEO of the American Association of Port Authorities (AAPA), pointed out that there was a critical need for investment in both land and waterside infrastructure, but said there was limited funding and waterfront land available for development. He said the ports and their private sector partners planned to invest more than $155 billion over the next five years in land and waterside (and digital) infrastructure, but that there needed to be more federal support.

“Our biggest concern from an investment standpoint is that the federal government down the road in Washington has not been upholding its part of the partnership in terms of investment in the landside and waterside connections in and out of the port facilities,” said Nagle. “We have identified $66 billion needed in federal investment in infrastructure over the next ten years.”

An added difficulty for Claussen was actually getting this message across and convincing legislators of the importance of the different types of ports in the US in supporting the country’s economy.

“People don’t really understand the economic importance of the different types of ports,” he said. Their importance was given a figure by Nagle, however, who noted that port cargo activities generated $321 billion in federal, state and local tax revenue.

Marad is working with the AAPA on a Port Planning and Investment Toolkit to help ports secure funding for infrastructure development. The toolkit contains modules to help ports properly plan for the development of infrastructure. It is also developing a port typology project using a GIS (geographic information system) to make clear what it is that the ports in the US are handling.

Kurt Nagle, CEO of the American Association of Port Authorities (AAPA)

Kurt Nagle, CEO of the American Association of Port Authorities (AAPA)Despite the shortfall in federal funding that Nagle pointed to, Claussen listed a number of grants and credit programmes that are available to the ports, including the surface transportation funding programme that is part of the US Department of Transport’s INFRA grant programme and makes $4.5 billion available, and the Transportation Infrastructure Finance and Innovation Act (TIFIA) Credit Program – just two of seven different programmes outlined in all by Claussen. In addition, the Port Conveyance Program transfers surplus federal land to states and local governments at no cost for use as a port facility.

Digital portsWith available land limited around the ports, stakeholders in the US need to improve the efficiency of throughput and that involves providing greater visibility over the vehicles being handled. For Kurt Nagle, that meant getting digital. He said port customers and stakeholders were looking for better visibility of their cargo – when it was going to arrive and where it was at any point in the supply chain – and meeting those needs was another way of highlighting the importance of the ports.

“Digitisation of data provides an opportunity for public ports authorities to show leadership in the trade community and provide avenues for that increasing flow of information,” said Nagle, adding that a number of major ports had developed digital platforms to provide customers with increased information and efficiency.

One example is the port of Los Angeles, which has worked with GE Transportation and last year introduced a cloud-based port optimiser that provides real-time information on cargo through a single portal that is made available to all the partners involved in the processing of it. According to GE Transportation, the system integrates data from across the port to better align people and resources and more efficiently move cargo through it. The port of Long Beach has since adopted it and the tool is available to other ports, according to Nagle.

That move toward collaborating on resources for the overall benefit of US port activity has also been seen in the marine cargo operating partnership between the ports of Tacoma and Seattle on the west coast of the US. The ports now operate in conjunction under the The Northwest Seaport Alliance.

Disruptive technology is also being used: Nagle pointed to a blockchain solution being used by Maersk as part of a joint venture with IBM. The port of Houston is also using blockchain in a pilot with US Customs and Border Protection. Nagle said using blockchain technology like this could increase international trade by 15%, which would feed into US port business, including for finished vehicles.

Potential of disruptionNew technology was certainly seen as the answer, with around half of delegates at the summit this year voting it the best opportunity for North American vehicle imports and exports above capital investment and US vehicle production.

Michael D’Angelo, manager of port operations for Volkswagen Group of America

Michael D’Angelo, manager of port operations for Volkswagen Group of AmericaMichael D’Angelo, manager of port operations for Volkswagen Group of America, focused on the potential disruptive technology offered to the sector and listed a number of industry-changing innovations that have taken off since 2007, including blockchain, which he noted had facilitated the secure sharing of information across multiple entities internationally. D’Angelo also pointed to autonomous vehicles and drones, and the model for vehicle production and sales that Tesla heralded.

However, he said the finished vehicle sector was generally lagging and that, save electronic proof of delivery (epod) and the odd “honourable mention” such as Audi’s autonomous parking robot ‘Ray’ in Ingolstadt, which can park 2,000 vehicles daily for rail transport, the sector was not leveraging the technology now available as quickly as it might.

Autonomy is helping in terms of yard management but it is a nascent concept in passenger vehicles, where demand from consumers does not match that for connected vehicles, according to Brad Miller, director of regulatory affairs and senior counsel of digital affairs at the North American Dealers Association (NADA).

He said there was a "hype cycle" on autonomy and, like any new technology, it would probably follow the predictable pattern drawn up by analysts including McKinsey and Gartner, which starts out with a huge wave of inflated expectations only to be followed by a dive into disillusionment before a more realistic take-up of the technology, when 3-5% of the market adopts it.

Nevertheless, there has been a lot of favour in government. Miller said many people in Washington DC had “drunk the KoolAid” on autonomous vehicles. The federal AV Bill, which found quick passage through the House, is now awaiting a final vote in the Senate, though opposition has now woken up and there could be challenges to its final approval as part of this summer’s Reauthorisation Bill.

Brad Miller, director of regulatory affairs and senior counsel of digital affairs at the North American Dealers Association (NADA)

Brad Miller, director of regulatory affairs and senior counsel of digital affairs at the North American Dealers Association (NADA)Autonomy will only have a real impact on the dealer business when it is combined with the various models associated with shared ownership, said Miller.

Lifespan logicWhat OEMs and their service providers needed to concentrate on in the meantime, according to VW’s D’Angelo, was an enhanced processing logic that looked at the entire lifespan of the vehicle to understand where it was coming from and where it had to go.

“We are really good at telling a customer where a car came from and where it is [at certain points] but we need to get better at telling the customer when the vehicle will get there,” said D’Angelo. “We want to move more toward advanced optimisation software. A lot of us are doing it but I think we can do it better.”

He highlighted the potential telematics not only in sharing information between the customer, the vehicle and the OEM, but also vendors involved in post-production accessorisation and value-added services.

“What vehicles can tell us is almost endless,” said D’Angelo. “Vehicles could tell when they needed a spoiler or doormat fitted, and that they would be at the dealer in three days.”

He added that in the interim, the sector needed to stop fighting for resources and share them more cleverly while developing that future technology.

GM’s intercontinental and port operations supervisor, Alrick Duncan, picked up on the use of technology to better serve the end customer and said the carmaker was looking at its own telematics service, OnStar, to bridge the gap between technology and customer service. Currently, GM can use the in-car function to locate a vehicle in a yard if it has gone missing on the system but there is greater potential ahead. Duncan said GM had also invested in providing options to the customer when it came to dealer pickups from its distribution centres and the ports.

At the moment, however, GM is working on visibility improvements based on the lead times it has built into the system. That was something Nissan was also doing, according to Bobby Hara, manager of import and export operations at Nissan North America. Regarding overseas deliveries, Hara said, there was variance and a carmaker only had a rough idea of the schedule.

“Once we receive [the vehicle] and we know we are going to get it we will provide an ETA [to the dealer] but it is broad and we don’t control the supply chain like FedEx or UPS,” said Hara, adding that those companies did not provide an ETA either until they had the product in their hands. “We have to rely on everyone involved to do their job.”

Duncan admitted that there had been delays in the delivery of vehicles made overseas (including South Korea) in the first quarter of 2018, which typically take 60-90 days to arrive but were delayed by capacity issues affecting the finished vehicle supply chain.

“In Q1, we faced a lot of problems because of a lack of rail cars and truck capacity, and that impacted across the network,” he said. “We saw longer lead times that definitely impacted our customers.”

A shortage of rail cars has forced some carmakers to deliver by road instead – though enclosed trucks can cost ten times as much

A shortage of rail cars has forced some carmakers to deliver by road instead – though enclosed trucks can cost ten times as muchRail headachesThe shortage of rail cars that hit the industry through 2017 and to an extent is still a problem in North America has had knock-on effects that have compounded the capacity problem. Faced with 30-day delivery times, carmakers have been opting for truck haulage, meaning that fewer trucks are available. For premium makes, using enclosed trailers to move vehicles by road can be ten times more expensive than rail, exacerbating logistics costs. Trucking a vehicle over 2,000 miles can also result in higher damage costs.

At the same time, carmakers are looking for opportunities to push more volumes onto rail – but for transport planners, better tracking and reliability on delivery time is needed.

Both Duncan and Hara said the rail providers needed to invest more in their asset programmes to deal with this because customers were looking for bigger vehicles, including SUVs and pick-up trucks, meaning that more bi-level wagons were needed.

This is something Anu Goel, executive vice-president, group after sales and services at VW Group of America, also picked up on, stating that vehicles getting bigger meant fewer being shipped per rail wagon or truck. That would make it more expensive to ship vehicles and the question was where that cost would be absorbed because shipment costs were not something the customer cared about.

At the same time, the rail providers have their own headaches, and some of these were discussed in the dedicated session on rail in one of four ‘Ideas Labs’ held at this year’s summit.

There is a mismatch between the multi-level equipment being used and that required by the rapid change in demand by customers for bigger vehicles. Getting the right equipment to the right place at the right time is made more problematic because OEMs are locating further from the markets in which they sell, with more cars being made in the south-east US and Mexico.

At the same time, there has been a proliferation of ports handling vehicles, with each OEM having their favourite location – something the rail providers cannot accommodate. There is also the aforementioned imbalance in imports and exports in the US and the basic seasonality of the automotive business, which is based on big peaks and troughs, creating a planning problem for everyone involved.

Jordan Kajifasz, managing director of sales and marketing at Canadian Pacific Railway, summed it up neatly by saying: “You are asked to build a church for Easter Sunday.”

Drivers go bigOn the mismatch between multi-level equipment and changing consumer habits, there has been a fundamental shift in segmentation between light trucks and passenger vehicles, according to figures from PwC Autofacts.

Brandon Mason, automotive director and mobility leader at PwC Autofacts

Brandon Mason, automotive director and mobility leader at PwC AutofactsBrandon Mason, automotive director and mobility leader at the company, said that back in 2012, there was roughly a 50:50 share between passenger vehicles and light trucks and the forecast under the Obama administration was for passenger vehicles to increase. Instead, the share in the US is now 70%-plus truck and 30% passenger vehicles.

“The original [fuel economy] target in 2012, when the CAFE standard was passed under the Obama administration, was 46.7 miles per gallon (mpg),” said Mason. “That is a moving target. At the time it was assumed it was going to be 54.5mpg by 2025. Given the fleet mix, that has come down significantly to 37mpg. At the time, they thought by 2025, two-thirds of the market would be passenger cars. It is just the opposite.”

The Trump administration is bringing in revisions to fuel economy standards that run counter to other major vehicle-making regions, notably China and the EU, where a regulatory framework designed to promote alternative propulsion vehicles means a more ready take-up of electric and hybrid vehicles. By around 2024, China and the EU are expected to each account for 30% of the global share of alternative propulsion vehicles (around 6.5m vehicles each), while Japan accounts for 20%, or about 4.5m. By then, the US is forecast to account for 11%, or 2.5m units, of the overall global share of alternative propulsion vehicles.

In fact, the US administration now in power is proposing a standard based on freezing emission and fuel economy assumptions from the 2020 model year. The Trump administration estimates that the number will work out to around 37mpg, give or take 10mpg, according to Mason.

[mpu_ad]Nevertheless, OEMs have said they want to forge ahead with alternative propulsion programmes, see how the situation plays out and adjust their fleets accordingly.

Trade warsOf course, one of the other big issues at this year’s summit in Baltimore was the potential impact of the Trump administration’s approach to trade, both in terms of the Nafta renegotiation with Canada and Mexico and further afield, with the continued threat of more tariffs on vehicle imports to the US and on US exports to markets including China.

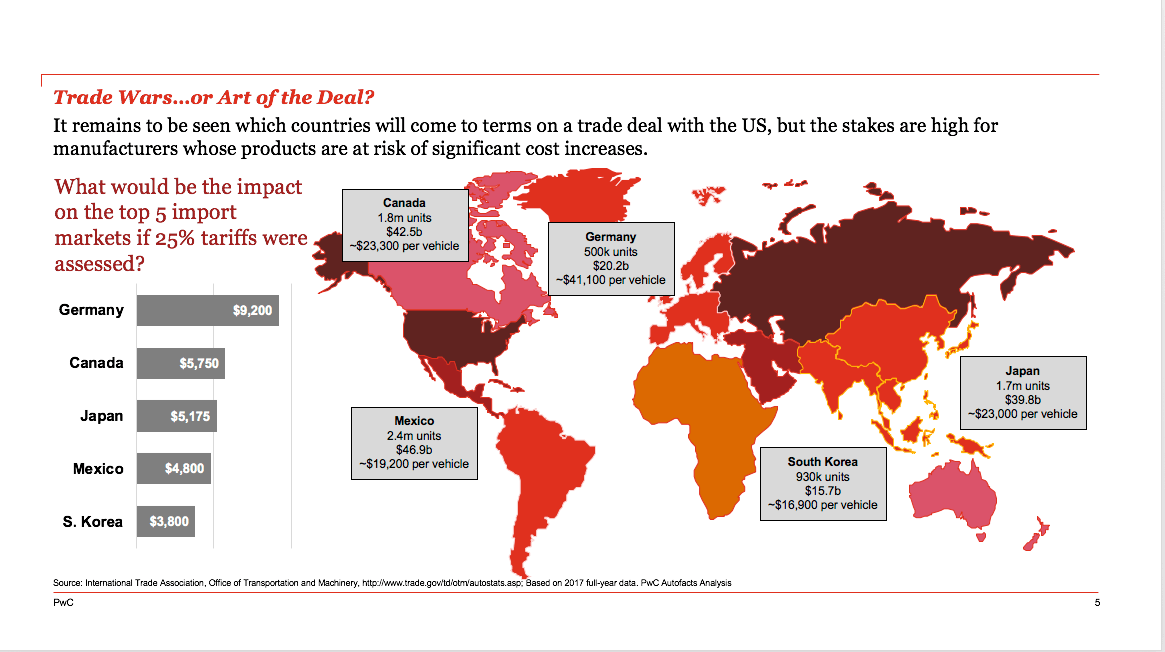

Among the delegates at the summit, 80% agreed that an all-out trade war with China would have either a highly or somewhat negative impact on business. PwC’s Mason conducted an ‘academic’ look at what it would look like if the US imposed a 25% tariff on all the vehicles it imported.

Currently Canada, Mexico and South Korea (under the KORUS agreement) do not pay any tariff on the vehicles they export to the US. Germany and Japan, meanwhile, have a 2.5% import tariff. China is off the list because the numbers are small: it sent about 65,000 vehicles to the US last year and the US sent about 270,000 to China.

However, according to PwC, the average additional price on the finished vehicle of a 25% tariff ranges from $4,000 for vehicles from Mexico to $9,000 for vehicles from Germany, the average price of those premium German vehicles already being $41,000 (see chart below).

Potential global impact of tariffs (click to enlarge)

Potential global impact of tariffs (click to enlarge)“At that point it is up to the OEM to decide whether to pass the cost on to consumers or eat the cost themselves,” said Mason.“We are already running slim on margins here and adding 25% is a pretty big pill to swallow. It is an academic exercise to speculate ...but there are some big dollars at stake here.”

Taking out the Nafta countries, there is still a trade imbalance. The US sends far more vehicles to China than China sends to the US, and China is the largest automotive market in the world. But in retaliation over Trump’s threat of import tariffs, China has said it will impose a 40% tariff on US vehicle imports.

“If you get a critical mass it makes a lot more sense to localise production there and forego the import tariff of 40%; the imbalance on light vehicles and parts is $4.3bn for China,” said Mason. The trade imbalance with Germany and the US would be $22 billion and with US-Japan it would be $52 billion, he added.

[related_topics align="right" border="yes"]The fact is the situation could go a number of ways and at this point, it is hard to make plans. Trump is well known for his particular brand of negotiating tactics and, according to Mason, it is unlikely that these are long-term, sustainable tariffs. From a strategy perspective, OEMs are unwilling to make big investments on what could be a short-term event, with trade negotiations set to continue and the prospect of a new government in the US in a couple of years.

Mason said some companies exporting to China had said they would absorb the cost for competitive reasons.

“If you suddenly have to pass on the cost of a tariff increase to a highly competitive market, your share will probably erode quickly,” he said. “But if it is a long-term play, you are likely to take your medicine as long as it lasts with a view to there being light at the end of the tunnel. A lot of companies are sitting tight to see what is actually going to happen over the long term.”

Finished Vehicle Logistics Import Export is part of the global Automotive Logistics series of conferences.

The next event, Automotive Logistics Global, will be held on September 18-20 in Detroit, USA.

Topics

- AAPA

- American Association of Port Authorities

- Asia

- Audi

- Canada

- Canadian Pacific Railway

- China

- Digitalisation

- Europe

- features

- Fedex

- Fedex

- Finished vehicle logistics

- General Motors

- Germany

- GM

- Japan

- Korea Rep

- Maersk

- Marad

- Mexico

- NADA

- Nissan

- Nissan

- Nissan North America

- North America

- North American Dealers Association

- Policy and regulation

- PwC Autofacts

- Rail

- Road

- Shipping

- Telematics

- Tesla

- United States Of America

- UPS

- UPS

- US Maritime Administration

- Volkswagen Group

- Volkswagen Group of America

- VW