State of Logistics 2021: 3PL

Challenged and in demand, 3PLs face transformation.

Given the challenges presented by the pandemic, shippers have leaned heavily on their third-party logistics (3PL) operators.

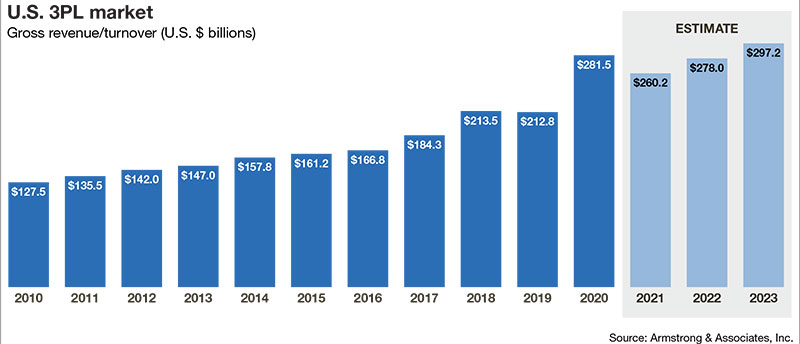

Subsequently, the industry has seen impressive growth. Estimates by Armstrong & Associates, Inc. (A&A) show U.S. 3PL market gross revenues grew 8.8% in 2020, bringing the total U.S. market to $231.5 billion.

“Most of that growth came from international and domestic transportation management, which responded to COVID-related demands for PPE and needs to restock inventories upon economic reopenings,” says Evan Armstrong, president of A&A.

In the meantime, Armstrong projects that revenue for 3PLs will stay strong throughout 2021, particularly in the domestic transportation management and freight brokerage sectors. “We’re currently estimating 20% growth by year’s end over 2020 and expect the overall 3PL market to see double-digit growth [12%+] in 2021,” he adds.

However, 3PL operators are not without their challenges. For one, development of the e-commerce sector and increases in demand for services that manage supply chains worldwide are expected to escalate.

Manufacturers and retailers are focusing more intensely on their core competencies and are now more readily subcontracting functions—such as logistics—to those with the expertise. Thus, the increase in competition has diverted the focus of manufacturers to promote respective specializations in production and distribution, according to a recent report from MarketWatch.

A recent survey conducted by Accenture and GEODIS of 200 large retail and consumer goods brands found that companies expect the shift to online sales—especially in selling directly on their own websites—to remain even after the pandemic subsides. “However, more than half [52%] believe that their logistics capabilities are not scaled to absorb quickly growing e-commerce

volumes,” stated the survey authors.

Consequently, 3PLs are going through a digital transformation and are investing in end-to-end solutions and end-to-end visibility to meet growing customer demand. And while these are all positive developments, it’s important to keep in mind that 3PLs work in an environment challenged by limited airfreight capacity, congested seaports, container shortages, and a trucking industry begging for more truck drivers.

“Shippers are wanting more committed capacity to combat rising spot market rates,” says Armstrong. “It has been especially difficult for companies that usually rely on load boards to move their freight.”

In a recent survey A&A conducted of top dedicated contract carriage providers, this continued and increasing capacity crunch has regular trucking fleets expanding into the dedicated contract sector and, to a greater degree, the dedicated truckload sector.

Therefore, A&A advises shippers to build application programming interfaces (APIs) with their top transportation management 3PLs to reduce tendering friction and more efficiently secure spot market truckload capacity. “Getter closer to 3PLs via technology is one way to better manage your supply chain and keep enough carrier capacity available to meet demand,” says Armstrong.

Today’s environment is also putting strains on warehousing, particularly given the enormous expansion of distribution centers by Amazon. “3PLs are seeing continued competition with Amazon on warehouse employee wages, so hiring and retaining employees, in addition to the effects the pandemic, have been challenging,” says Armstrong.

In addition, low warehouse vacancy rates, on top of rising lease rates, especially in key distribution areas, continue to increase costs for the 3PL—and then ultimately the shipper.

With all of these challenges rolled up, Armstrong projects that 3PLs should see more modest growth in 2022, with activity returning to normal. “Shippers should expect fewer challenges and more stable conditions over the next year,” he adds.

View the other 2021 State of Logistics topics here.

Article Topics

3PL News & Resources

Shipment and expenditure decreases trend down, notes Cass Freight Index March trucking tonnage trends down, reports ATA FTR Shippers Conditions Index enters negative territory DAT March Truckload Volume Index sees modest March gains National diesel average, for week of April 22, is down for the second straight week UPS reports first quarter earnings decline LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics More 3PLLatest in Logistics

Shipment and expenditure decreases trend down, notes Cass Freight Index March trucking tonnage trends down, reports ATA FTR Shippers Conditions Index enters negative territory DAT March Truckload Volume Index sees modest March gains National diesel average, for week of April 22, is down for the second straight week UPS reports first quarter earnings decline LM Podcast Series: Assessing the freight transportation and logistics markets with Tom Nightingale, AFS Logistics More LogisticsSubscribe to Logistics Management Magazine

Find out what the world's most innovative companies are doing to improve productivity in their plants and distribution centers.

Start your FREE subscription today.

April 2023 Logistics Management

Latest Resources